| |

Operating results

Introduction

During 2009, changes were made to the Group’s internal reporting structure to assist the Board in focusing on the performance of the Group’s ongoing businesses. Distinction is now drawn between those of the Group’s continuing operations that are ongoing and those that have been exited but do not meet the conditions to be classified as discontinued operations. An explanation of the changes is provided in note 4 to the consolidated financial statements. Comparative information for 2008 and 2007 has been re-presented to reflect these changes.

At the beginning of 2009, we adopted an amendment to IFRS 2 ‘Share-based Payment’. Comparative figures presented throughout the Operating and Financial Review have been restated to reflect the retrospective application of the amendment, which had the effect of reducing the Group’s operating profit by $0.5 million in 2008 and by $0.3 million in 2007.

We assess the financial performance of our businesses using a variety of measures. Certain of these measures are particularly important and we have termed them ‘key performance measures’. We refer to these key performance measures, which include ‘non-GAAP measures’, throughout the Operating and Financial Review. An explanation of each key performance measure is provided in Explanation of key performance measures. Reconciliations of operating profit to adjusted operating profit for the Group as a whole and for each ongoing segment, and an analysis identifying the underlying change in sales and adjusted operating profit for each ongoing segment are presented in Explanation of key performance measures.

2009 compared with 2008

Continuing operations

|

|

|

2009 |

|

|

|

2008 |

|

|

|

|

|

|

|

|

| $ million, unless stated otherwise |

Ongoing

segments |

Exited

segments |

Total |

|

Ongoing

segments |

Exited

segments |

Total |

|

|

|

|

|

|

|

|

| Sales |

|

|

|

|

|

|

|

| Industrial & Automotive |

3,129.1 |

– |

3,129.1 |

|

3,980.6 |

80.2 |

4,060.8 |

| Building Products |

1,014.5 |

36.5 |

1,051.0 |

|

1,320.5 |

134.6 |

1,455.1 |

|

|

|

|

|

|

|

|

| Total |

4,143.6 |

36.5 |

4,180.1 |

|

5,301.1 |

214.8 |

5,515.9 |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

| Adjusted operating profit/(loss) |

|

|

|

|

|

|

|

| Industrial & Automotive |

226.1 |

– |

226.1 |

|

349.4 |

10.3 |

359.7 |

| Building Products |

69.1 |

(13.1) |

56.0 |

|

92.4 |

(12.2) |

80.2 |

| Corporate |

(32.3) |

– |

(32.3) |

|

(37.0) |

– |

(37.0) |

|

|

|

|

|

|

|

|

| Total |

262.9 |

(13.1) |

249.8 |

|

404.8 |

(1.9) |

402.9 |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

| Adjusted operating margin |

|

|

|

|

|

|

|

| Industrial & Automotive |

7.2% |

– |

7.2% |

|

8.8% |

12.8% |

8.9% |

| Building Products |

6.8% |

(35.9)% |

5.3% |

|

7.0% |

(9.1)% |

5.5% |

| Total |

6.3% |

(35.9)% |

6.0% |

|

7.6% |

(0.9)% |

7.3% |

|

|

|

|

|

|

|

|

Sales

Sales from continuing operations were $4,180.1 million (2008: $5,515.9 million), a decline of 24.2%. Most of the Group’s end markets weakened significantly, particularly in the first half of the year, which caused a corresponding decline in sales volumes across the Group. Sales fell by $247.4 million compared with 2008 due to changes in average currency exchange rates. Sales were reduced by $79.5 million due to the disposal of Stant and Standard-Thomson, but this was partially offset by the contribution of recent acquisitions which added $26.4 million to sales compared with 2008. On an underlying basis, sales were down $1,035.3 million, or 20.0%, compared with 2008. |

|

|

Cost of sales

Cost of sales was $2,995.9 million in 2009 compared with $4,023.7 million in 2008. Cost of sales may be analysed as follows:

| $ million, unless otherwise stated |

2009 |

2008 |

|

|

|

| Inventory brought forward |

772.4 |

799.8 |

|

|

|

| |

|

|

| Production costs incurred: |

|

|

| – Raw materials |

1,519.7 |

2,326.5 |

| – Direct labour costs |

317.9 |

462.2 |

| – Other direct costs |

128.3 |

201.1 |

| – Depreciation |

153.5 |

183.7 |

| – Other overheads |

661.5 |

878.5 |

|

|

|

| |

2,780.9 |

4,052.0 |

| Acquisitions |

7.5 |

12.4 |

| Disposals |

– |

(16.8) |

| Currency translation differences |

25.9 |

(51.3) |

|

|

|

| |

2,814.3 |

3,996.3 |

|

|

|

| Inventory carried forward |

(590.8) |

(772.4) |

|

|

|

| Cost of sales |

2,995.9 |

4,023.7 |

|

|

|

| |

|

|

| Gross margin |

28.3% |

27.1% |

|

|

|

During 2009, the Group reduced its production levels in response to declining sales volumes and in order to reduce inventory in support of management’s continuing effort to control working capital levels. Also during 2009, the Group benefited from reductions in its cost base resulting from projects Eagle and Cheetah. Due to the combination of these factors, raw material, direct labour and other direct costs incurred each declined by more than 30% in 2009 compared with 2008. Depreciation was 16.4% lower than in 2008, reflecting the impact of restructuring initiatives during 2009, the impairment of property, plant and equipment that was recognised in 2008 and management’s strict control over capital expenditure levels. Other overheads incurred were 24.7% lower than in 2008.

Overall, the gross margin increased from 27.1% in 2008 to 28.3% in 2009.

Distribution costs

Distribution costs were $464.8 million in 2009 compared with $584.5 million in 2008, down 20.5%. Distribution costs fell in response to lower sales volumes and lower energy costs.

Administrative expenses

Administrative expenses were $480.4 million in 2009 compared with $513.3 million in 2008, down 6.4%. Administrative expenses declined principally due to headcount reductions, lower property costs and reduced professional and consultancy fees.

Impairments

In 2009, the Group recognised impairments amounting to $73.0 million, comprising $18.9 million on goodwill and intangible assets arising on acquisitions, $38.6 million on assets that have become impaired as a consequence of the Group’s restructuring initiatives and $15.5 million on receivables held in relation to the disposal of businesses in prior years.

In 2008, impairments amounted to $342.4 million, of which $228.6 million related to goodwill and $113.8 million to property, plant and equipment, largely as a result of the significant deterioration during 2008 of the North American automotive OE and US residential construction markets.

Restructuring costs

Restructuring costs arise from major projects undertaken to rationalise the Group’s operations and to improve its cost competitiveness.

In 2009, restructuring costs amounted to $144.1 million and principally related to the restructuring of the Group’s manufacturing operations under projects Eagle and Cheetah. We expect to recognise further costs of approximately $12 million and a net cash outflow of approximately $65 million to complete these projects in 2010.

In 2008, restructuring costs were $26.0 million and largely related to the closure of manufacturing facilities and the outsourcing of information technology services.

Net gain on disposals and on the exit of businesses

During 2009, the Group recognised a net gain of $0.2 million in relation to the disposal of businesses in prior years. In 2008, a gain of $43.2 million was recognised on the disposal of Stant and Standard-Thomson.

Gain on amendments to post-employment benefit plans

With effect from 30 September 2009, the Group closed its principal defined benefit pension plans in the US and Canada to future service accrual and the deferred pension benefits accrued under those plans were frozen, based on the pensionable salaries of participating employees at that date. In addition, the Group closed the Gates post-retirement healthcare plan in the US to employees who had not retired by 31 December 2009 and reduced the benefits payable to existing beneficiaries.

As a result of these amendments, the Group recognised a gain of $63.0 million, of which $35.3 million related to pensions and $27.7 million to healthcare benefits.

Share of loss of associates

In 2009, the Group’s share of the loss after tax of its associates was $0.4 million (2008: loss of $2.1 million).

Operating profit

Operating profit was $84.7 million in 2009 compared with $66.9 million in 2008.

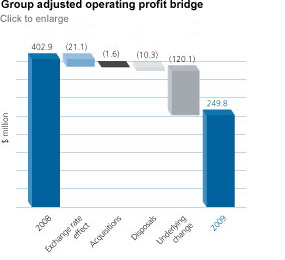

Adjusted operating profit was $249.8 million (2008: $402.9 million), down 38.0%, due largely to the effect of reduced sales volumes. Adjusted operating profit fell by $21.1 million compared with 2008 due to changes in average currency exchange rates, principally the weakening of sterling and the Mexican peso against the US dollar. Disposals reduced adjusted operating profit by $10.3 million compared with 2008. On an underlying basis, adjusted operating profit was down $120.1 million, or 32.3%, compared with 2008.

The Group’s adjusted operating margin was 6.0% in 2009, compared with 7.3% in 2008. Although the margin fell in the first half of 2009, it recovered in the second half of the year, reflecting the effect of improving sales and the reduction in the Group’s cost base that has resulted from our restructuring initiatives. |

|

|

General price inflation in countries where the Group has its most significant operations remained at a low level during 2009 and the impact of inflation was not material to the Group’s operating results.

Net finance costs

Net finance costs were $46.3 million (2008: $75.0 million). Net interest payable on net borrowings was lower at $38.6 million (2008: $47.1 million) due to lower average net debt and lower average interest rates during 2009 compared with 2008.

In 2009, the net finance cost recognised in relation to post-employment benefits was $7.4 million (2008: $2.9 million) as follows:

| |

2009

$m |

2008

$m |

|

|

|

| Interest cost on benefit obligation |

70.0 |

78.4 |

| Expected return on plan assets |

(62.6) |

(75.5) |

|

|

|

| Net finance cost |

7.4 |

2.9 |

|

|

|

Other finance expense was $0.3 million (2008: $25.0 million), which principally related to gains and losses on financial instruments held by the Group to hedge its currency translation exposures that either did not qualify for hedge accounting or in respect of which there was hedge ineffectiveness.

Income tax expense

In 2009, the income tax expense attributable to continuing operations was $28.5 million (2008: $38.4 million) on a profit before tax of $38.4 million (2008: loss before tax of $8.1 million).

After adjusting for the items excluded from operating profit in arriving at adjusted operating profit and the tax attributable to those items, the income tax expense was $51.0 million (2008: $80.8 million) on a profit before tax of $203.5 million (2008: $327.9 million). On this basis, the Group’s effective tax rate was 25.1% (2008: 24.6%) and is expected to be approximately 25% in 2010.

Minority interests

In 2009, the profit after tax attributable to minority shareholders in subsidiaries not wholly-owned by the Group was $21.6 million (2008: $18.1 million).

(Loss)/earnings per share

In 2009, there was a loss from continuing operations attributable to equity shareholders of $11.7 million (2008: loss of $64.6 million) and the loss per share from continuing operations was 1.33 cents (2008: loss per share of 7.34 cents).

Earnings for the purposes of calculating adjusted earnings per share are adjusted for the items excluded from adjusted operating profit and the tax attributable to those items. On this basis, there was a profit from continuing operations attributable to equity shareholders of $130.9 million (2008: $229.0 million). Adjusted diluted earnings per share were 14.81 cents (2008: 25.96 cents).

Dividend

The Board proposes a final dividend for 2009 of 6.50 cents per share, which, based on the number of shares currently in issue, will amount to $57.4 million. When taken together with the interim dividend of 3.50 cents per share that was paid in November 2009, the total dividend proposed for 2009 is 10.00 cents per share (2008: 13.02 cents per share). The Board will seek to resume its progressive dividend policy as soon as the Group’s results and market conditions allow. |

|