|

TONY HOLT UNDERWRITING DIRECTOR

TONY HOLT UNDERWRITING DIRECTOR

“The combination of Amlin’s underwriting expertise

and a consistent philosophy of delivering gross

underwriting profits is an extremely important

differentiator of Amlin from its peers.”

|

|

To find out more about catastrophe modelling, please click here

To find out more about Amlin's Dynamic Financial Analysis Model click here

There are many aspects to the formulation

of a strong underwriting philosophy and it is

important to get it right at a strategic portfolio

level and also at a detailed transactional level.

The key aspects of Amlin’s philosophy are

summarised below.

|

|

| PROFIT FOCUS |

|

Underwriting, and particularly the ability to

assess and price risk, is a critical skill set for

Amlin. The Group aims to deliver an underwriting

profit from each class of business in every year

of underwriting. The importance of this to

Amlin is emphasised constantly in the planning,

execution and review of our underwriting. It is

understood that to produce adequate returns

on capital the Group cannot rely solely upon

investment returns from premiums written,

and that combined ratios must be low enough

to generate underwriting returns through the

insurance cycle.

|

|

| DIVERSITY |

|

Amlin’s portfolio of business is diverse by type

or class of insurance and territorial scope. We

aim to balance potentially volatile catastrophe

type classes such as catastrophe reinsurance or

energy with less volatile classes such as motor

or marine cargo. This diversification provides

us with returns from several independent lines

of business which have limited correlation in

terms of loss experience and pricing within

the market cycle. Analysis carried out on our

portfolio using our Dynamic Financial Analysis

(“DFA”) modelling tool shows the strong benefits

of this diversification on our risk profile.

|

|

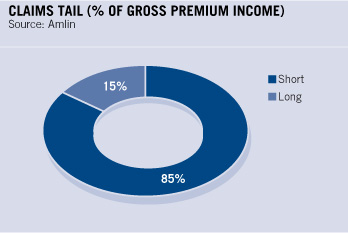

| SHORT TAIL FOCUS |

|

Our portfolio is biased in favour of short tail

risk. This means that for a very large part of our

portfolio we will have a high level of confidence

in the expected quantum of claims within 18

months of the expiry of each risk. The

advantage of this is that we are able to assess

any repricing needs faster than in respect of

longer tail risks. We will also be less prone to

the reserving difficulties which still plague so

many in the industry.

The long tail risk that we underwrite is focused

in areas where good actuarial modelling can

help determine an acceptable price for risk

or where the risk is catastrophe related, with

claims arising from accidents rather than

disease. We have a negligible involvement

in areas such as Directors’ and Officers’

insurance, where systemic developments can

arise, resulting in significant claims, the risk

of which is not capable of proper evaluation

at the time of pricing the risk.

To find out more about catastrophe modelling, please click here

To find out more about Amlin's Dynamic Financial Analysis Model click here

|

|