|

|

|

|

|

|

OPERATING AND FINANCIAL REVIEW / THE COMPANY / DELIVERING VALUE /

|

| EXPERIENCE |

|

The classes of business written have been

developed over many years and new products

are not launched without significant

investigation. Even then, the premium income

capacity allocated to a new class would

initially be low and the profile of the class

would be built up slowly and carefully over

several underwriting years in order to build

confidence and knowledge. Therefore the bulk

of the premium income written is on business

where Amlin has strong knowledge, expertise

and historical data. This assists in the planning

and modelling of potential outcomes.

|

|

| CYCLE MANAGEMENT OF VOLUME |

|

Amlin has a premium income capacity

allocated to each line of business for each

calendar year, but these are not targets. It is

clear for all underwriting staff that underpriced

business is to be declined and that gross

underwriting profit takes precedence over

volumes of business. For the syndicate as a

whole, this philosophy can be seen in the

reduction in gross premium income and market

share during the environment of soft pricing.

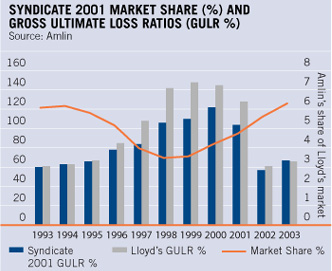

The graph above shows an analysis of the

underwriting performance, as measured by

gross ultimate loss ratios at 31 December

2003, of Amlin’s ongoing business over the

period 1993 to 2003.

The orange line shows Amlin’s own market

share as a percentage of the market over

the same period. There are three important

conclusions that can be drawn from this chart.

First, Syndicate 2001’s ongoing business has a

record of strong outperformance across the

cycle. Second, that outperformance is most

strongly visible when market conditions are

most difficult and overall loss ratios are poor.

Third, that Amlin’s market share is highest

when market conditions are at their most

favourable and, conversely, market share

is lowest when loss ratios are at their worst.

|

|

|

|

|

|

|

|

|

|

|